Global investment banks have cashed in on the Adani Group’s voracious appetite for debt. Now their client is accused of pulling off ‘the largest con in corporate history’

Last summer, after the Adani Group completed its US$10.5 billion leveraged buyout of a cement business from Swiss firm Holcim, Gautam Adani, the conglomerate’s mastermind and then world’s fifth richest man, boasted to the Economic Times that his “relationship banks” – Barclays, Deutsche Bank and Standard Chartered Bank – had “fully funded” the deal.

Those relationships may come under strain, following the publication of short seller Hindenburg Research’s explosive 32,000-word report, which alleges that the Adani Group and its principals have engaged in a years-long scheme of fraud and stock market manipulation. (The Adani Group has denied all wrongdoing and says it is considering legal action against the investment firm.)

Founded in the 1980s as a commodities trading firm, the Adani Group has grown into a US$23 billion (annual sales) conglomerate with seven publicly-traded firms involved in energy, industrial and logistics businesses across India. The family-run enterprise has close ties to Prime Minister Narenda Modi, and its access to loans from Indian banks has largely funded the firm’s acquisition-driven growth.

In recent years however, U.S and European-based investment banks have stepped up to help the Adani Group raise billions of dollars through equity sales, refinancings and U.S. dollar debt offerings. In addition to the Adani Group’s “relationship” banks, J.P. Morgan, Bank of America Merrill Lynch and Credit Suisse have all brokered deals on behalf of Adani-owned companies.

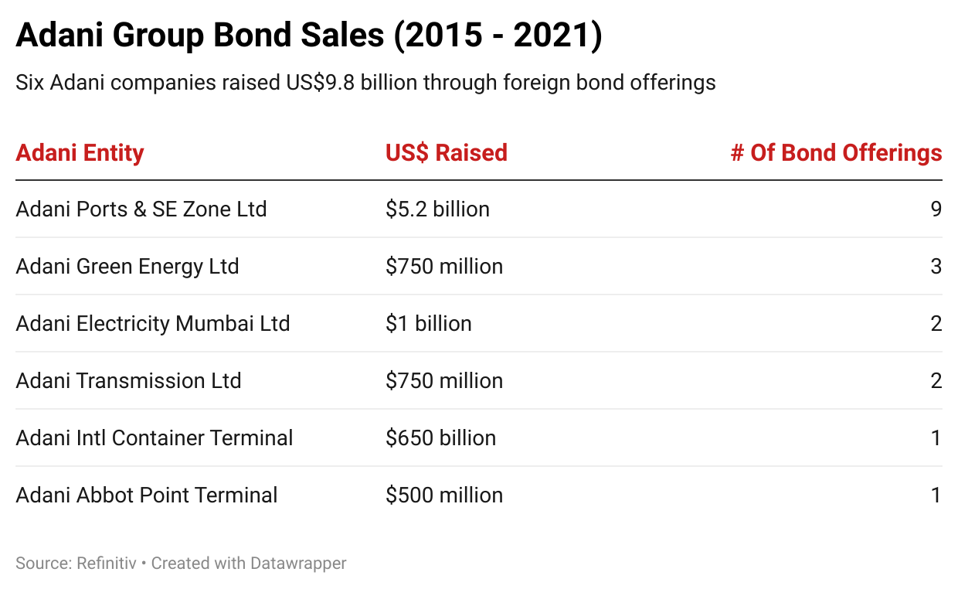

Between 2015 and 2021, six different Adani Group companies raised about US$10 billion through U.S-dollar-denominated bond sales that were underwritten by U.S. and European investment banks, according to financial market data provider Refinitiv. Of these 18 bond offerings, 14 were done between May 2019 and September 2021. One of these companies, Adani Ports & Special Economic Zone – which receives preferential tax treatments – was responsible for half the debt raised.

These figures do not include the Adani Group’s debt issued in Rupees and other currencies. The conglomerate had about US$27 billion in outstanding liabilities as of March 2022. The State Bank of India provided funding for about 40% of debt Adani firms issued between 2020 and 2022.

Forbes

Leverage is at the heart of Hindenburg Research’s fraud allegations. The Adani Group companies and Adani-owned offshore shell companies lend each other money as a way to launder money and cook their books, Hindenburg alleges. Hindenburg homed in on several loans between Adani entities, including a US$253 million loan from a Mauritius-based shell company – which appears to be controlled by Guatam Adani’s brother, Vinod Adani – to a private Adani-owned entity, which then lent US$138 million to Adani Enterprises, a publicly traded company. In another instance, Emerging Market Investment DMCC, a United Arab Emirates-based entity with virtually no online presence, inexplicably had US$1 billion, which it lent to Mahan Energen, a subsidiary of Adani Power.

“It’s a house of cards, it’s all fueled on debt,” one anonymous employee of Elara India Opportunities, a London-based company that manages various funds invested in Adani companies, told Hindenburg.

Concerns about the Adani Group’s debt load have long shadowed the company. In 2019, Indian news outlet Scroll.in published an investigation on Adani Group’s web of related party deals, including how Adani-owned entities “saw multiple transfers of money between themselves in the form of loans and repayments.” Fitch Group’s CreditSights group published a report last year warning that the Adani Group is “deeply overleveraged.”

Adani has a knack for securing investor funds. “My projects are immensely bankable,” he told Forbes Asia back in 2014. The conglomerate’s focus on real infrastructure projects – with their reliable cash flows – were part of the draw. “Banks are willing to take a long-term view as these are much required assets for the country with assured returns,” K. Shankar, a power analyst at Edelweiss Capital, a financial services firm in Mumbai, told Forbes at the time.

Wall Street only began to really warm up to Adanis when he sought financing for Adani Green Energy, the conglomerate’s renewable energy subsidiary, according to Tim Buckley, a former investment banker at Citigroup and director at Australia-based Climate Energy Finance, who has been studying the Adani Group for over a decade. Money raised by Adani Green Energy or Adani Ports may “just get transferred to Adani Power and Adani Enterprises, and then goes towards building more coal fired power plants or more coal mines,” Buckley says.

As of June 2021, over US$420 million of Adani Green Energy shares were owned by a Cyprus-based entity, New Leaina Investments, which allegedly is owned by Adani Group executives, according to Hindenburg. That offshore holding effectively allowed Adani Green to skirt Indian regulations that require listed companies to maintain a non-promoter public float of at least 25%, alleges Hindenburg.

The Adani Group’s plan to develop the world’s largest coal mine in Australia provoked the Stop Adani campaign. J.P. Morgan, Bank of America Merrill Lynch, Credit Suisse, Barclays, Standard Chartered and Deutsche Bank have all sworn off financing the controversial project, though all appear to still be doing business with the parent group.

“Adani’s involvement in massive new thermal coal mines in the midst of the climate crisis hasn’t been enough to convince some major banks such as Deutsche Bank, Standard Chartered and Barclays to cut ties,” says Pablo Brait, a campaigner at Australian environmental finance organization Market Forces. “Hopefully these significant allegations will finally help all banks wake up to the risks of financing Adani.”

It remains to be seen how bankable Adani will be in the months ahead. Barclays, Deutsche Bank, JP Morgan and Bank of America all declined to comment on their relationship to the Adani Group. Standard Chartered Bank said it doesn’t comment on client relationships due to confidentiality. And Credit Suisse had not responded at the time of publication.