The new home of the mixed martial arts UFC and wrestling’s WWE – inside a company known as TKO Group Holdings – went public this week to great fanfare, but there is massive debt that needs to be refinanced by 2026.

TKO Group Holdings, the newly merged business operations of UFC and WWE that began trading Tuesday, has had an unspectacular start. The share price has slipped $1, to $101, since its initial public offering.

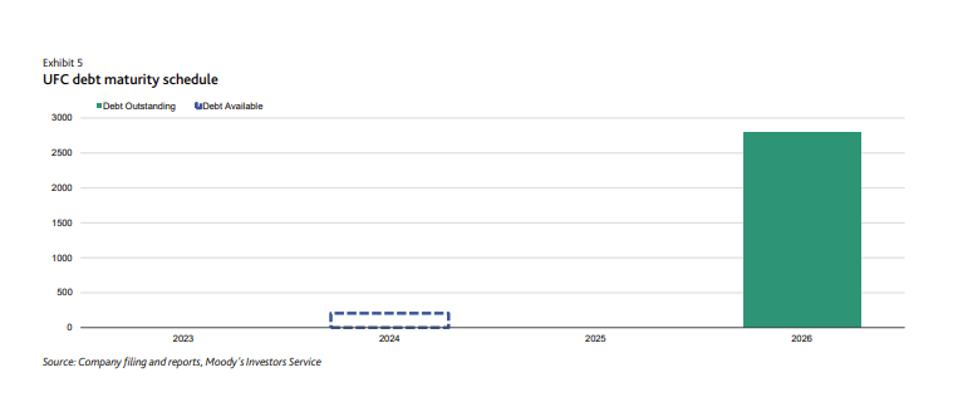

The big concern, it seems, is that TKO is highly leveraged, with $3.2 billion of debt, supported by about $1.2 billion of EBITDA for 2023. Even more ominous, TKO has less than three years to deal with a ticking time bomb: $2.7 billion of UFC debt due in 2026.

This would be an overreaction. Yes, refinancing the debt will be more expensive. As the prospectus on the merged company states: “Because borrowings under the UFC Credit Facilities bear interest at a variable rate, UFC’s interest expense could increase, exacerbating these risks. The Federal Reserve has recently raised, and may in the future further raise, interest rates to combat the effects of recent high inflation. Increases in these rates may increase UFC’s interest expense. For example, for the year ended December 31, 2022, UFC’s interest expense experienced a net increase of $37.3 million, or 36.5%, compared to the year ended December 31, 2021, primarily driven by higher interest rates on UFC’s variable rate indebtedness that was partially offset by lower overall indebtedness. … Based on the outstanding indebtedness under the UFC Credit Facilities as of December 31, 2022, a hypothetical 100-basis-point increase in interest rates would have resulted in an approximately $28 million increase in annual interest expense.”

That said, this should not be a reason to avoid owning shares of TKO. In fact, Moody’s Investors Service is actually considering upgrading the company’s UFC’s B2 Corporate Family Rating. Why? The ratings agency writes, in part: “Our review for upgrade considers the enhanced scale arising from the combination, higher operating leverage and greater business diversity. We believe the combination of WWE and UFC will create an entity with a larger devoted fan base across several geographies, providing the new company the ability to maximize the value of its media rights and sponsorships. With upcoming contracts set to expire over the next few years with media companies like Fox, NBCUniversal and the Walt Disney Company, the combination offers additional leverage and better position the new company to monetize its content across multiple platforms.”

Mark Shapiro, TKO’s president and chief operating officer, said in a recent interview with CNBC that the company aims to make acquisitions and expand beyond combat sports. This makes sense as the differences between sports, entertainment and lifestyle brands blur even further, and sports empires that can create platforms with scale dominate entertainment.

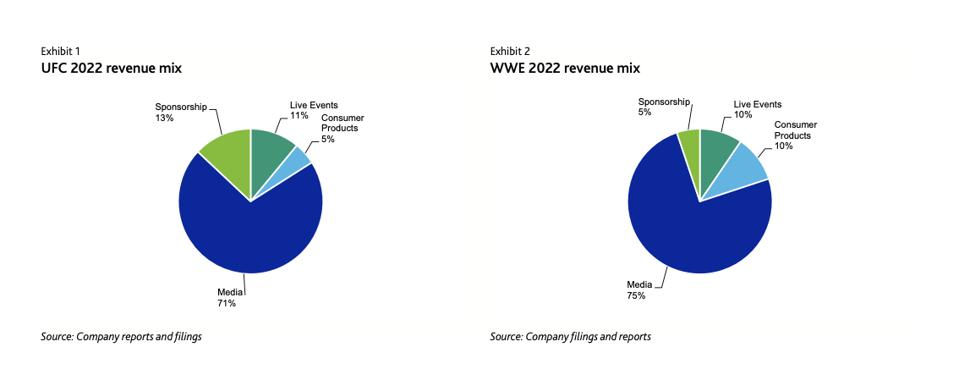

A recent report by Seaport Research Partners concurs, noting: “The key synergies should come from Endeavor’s knowledge of rights pricing around the globe (by virtue of EDR executives and agents having sat at both sides of the negotiating table), and with easier access to a wide array of media distribution and sponsorship partners. WWE has likely already been in negotiations related to its September 2024 expiration of contracts with Comcast (USA Network and Peacock) and Fox, which have a combined annual average value of about $520 million, we estimate (including the developmental wrestlers’ program NXT). We think as a base case, if NXT is excluded and gets wrapped into the separate Peacock/WWE Network deal that expires in 1Q26, could be a 40% increase in the average annual value (or a 15% step-up in Year 1 vs. Year 5 of the old deal), or $190 million annually on average.”

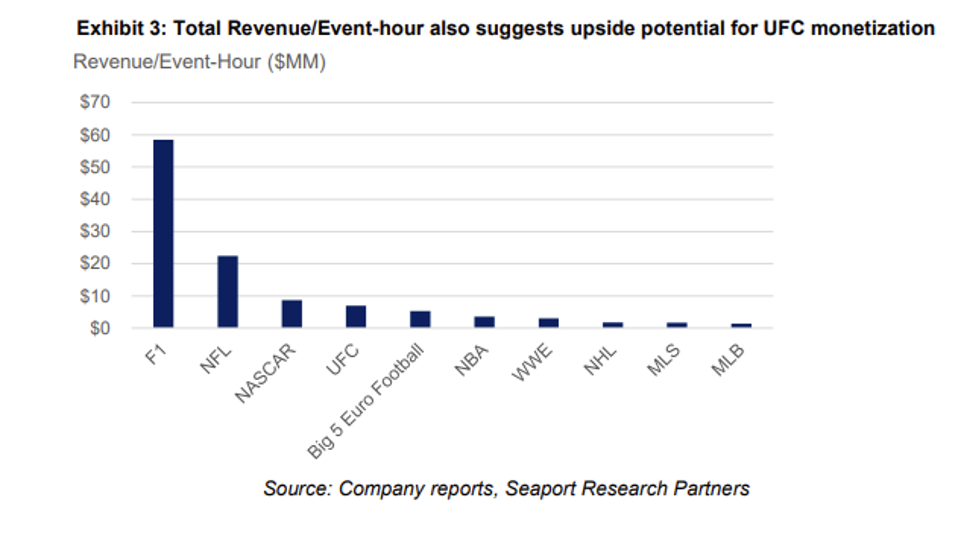

As for UFC, Seaport believes the MMA promotion has an opportunity to generate significantly more revenue per event, which should ease some of the concerns about its debt.

This article was originally published on forbes.com and all figures are in USD.