Schroders head of fixed income, Kellie Wood, has been in markets for more than 25 years and has had a pivotal role in building her firm’s domestic fixed income business. She spoke to Stewart Hawkins about how the defensive asset class is redefining its role amid a new market paradigm, the risks of geopolitical volatility, how gold has glittered and why she’s not really keen on Australian stocks.

How have you been building wealth for your clients over the past decades? What’s been your guiding principle?

As a fixed-income investor, it’s certainly been anchored in several key points, but firstly, striking the right balance between generating high-quality income and preserving capital in the defensive asset space.

Do you consider fixed income to be fundamentally a defensive asset?

In the new regime, I think fixed income is redefining its place in portfolios.

We’ve entered this environment where growth and inflation is structurally higher, and central banks will keep interest rates structurally higher. Sovereign debt levels at the moment, on average, in the developed world are about 100% of GDP.

We’re in this environment where central banks and governments need to run economies hot. What that means is keeping growth rates higher and keeping inflation stickier to grow themselves out of this debt. In that environment with interest rates staying structurally higher, bonds haven’t been a good diversifier of equity risk… because we’ve been in soft landing and reflation (phases).

That’s why bonds have had to redefine their role in portfolios, being now a place to go to deliver high levels of income, but also a return. You think about some of the credit funds over the last few years, they’ve delivered between 10 and 15% returns for much lower levels of risk than equities. We’re not constructing fixed-income portfolios to diversify against equity risk because we believe we’ll remain in this reflationary environment. The role fixed income plays in that environment is very different to what we saw in the Global Financial Crisis (GFC) decade.

Post GFC, basically, you had free money. How has this situation evolved?

The regime has changed because of the mix of growth and inflation. If you think back to that GFC decade, that was an environment where growth was low, inflation was low, and central bank

policy was low; we had endless amounts of quantitative easing. Central banks continued to try to stimulate growth rates.

[We had] negative interest rates, but a huge amount of fiscal austerity. That’s where you had very firm negative correlations between bonds and equities because bonds were continuing to move down as central banks continued to pressure bond rates. [Now] we’ve higher growth, we have higher inflation, the correlation between bonds and equities is very unstable and/or more positive, and that’s one of the reasons why bonds haven’t been a good diversifier of equity risk. I’m talking specifically about government bonds because central banks have had to keep policy tight. If you think back to that GFC decade, it was an environment where we saw a huge chase for yield because yields were so low.

That’s where we saw the huge development of the private debt market because there was yield in private debt, not in public debt. And we saw a huge move towards passive investing, where we’re now seeing very good value in public debt markets versus private markets. If you look at even our high-yielding credit fund over the past three years, [it] has delivered the same returns [as] you’re getting in the private credit space. Higher quality, shorter maturity profile. So you’re not getting compensated for illiquidity, like the vagueness in private credit. The other shift we’re seeing is the move back towards active [investing]. We look at the funds we run, primarily our top-down fixed-income and multi-asset portfolios. Last year, even the past few years, we have made the best returns seen in over a decade.

What does that mean for the Australian investor investing in AUD in the fixed-income space?

Having the ability to access the diversity of the global fixed income markets, utilising that breadth, and having a flexible mandate can deliver you far superior risk-adjusted returns. If you look at the returns just in this year, the best-performing asset class in fixed income globally has been emerging market debt. [In the year to December 2025], it’s produced about 15%.

Those 15% returns were more angled towards sovereign [debt] because you had very high real yields in most of the emerging markets, and you’ve had the benefit of the US dollar falling through most of 2025. We’ve seen very strong returns across Australian, European, and US credit markets, both investment-grade and high-yield. It’s certainly been an environment where it’s paid to be long risk, whether that’s been in equities, credit, or alternatives.

What about market volatility? Geo-politically, at least, aren’t we in “interesting times”?

Well, there are several drivers. I think it’s just general geopolitical fragmentation. We saw this with Liberation Day in terms of the Trump administration and the impact of tariffs and just general uncertainty. What [does] that ultimately mean for growth and inflation for different economies?

We’ve entered this whole new dimension of fiscal dominance. And this is where countries are spending more money on security, defence, cost of living, climate change, aging, demographics, which are here to stay. The fact that we’ve got monetary policy volatility alongside this environment of just fiscal dominance, governments’ spending in terms of where they want to be allocating capital within economies, alongside tariff uncertainty, and general geopolitical fragmentation. It’s those four things I will point to that are really creating this macro volatility. It’s less about valuations. We all know equities have been pretty expensive for some time.

But much of this fiscal dominance is being funded by debt.

Yes. And this brings me back to my original comment: economies need to be run hot because of structurally high debt levels. The biggest risk out there to markets is an environment where we do start to move down into… slow down, recession, stagflation, because in that environment, we have growth slow, we have inflation remaining sticky, which means central banks cannot continue to ease policy rates to support growth because inflation is re-accelerating. That is where, if growth falls below the rate of interest, the debt is not sustainable. Then we’re potentially looking at a sovereign financial crisis.

Is this your doomsday scenario?

Yeah. This is the doomsday.

If central banks and governments don’t continue to expand and run these economies hot, and growth actually really starts to slow at a point where inflation is re-accelerating, then that is a big problem because of the level of debt in economies in the government sector.

Talk me through what you’re doing now?

As a general comment, equities are expensive, so your growth portion of your portfolio is expensive, or valuations are stretched, and your defensive portfolio, government bonds, have not been a good diversifier of equity risk in this reflationary environment.

What we have been doing within our broader multi-asset portfolios is building in genuine diversification. What I mean is uncorrelated drivers of returns. This is making better use out of asset classes like emerging-market sovereign debt… [and]… like investment grade credit [developed market], so like Triple B corporates and hybrids, which is predominantly our

high-yielding credit fund.

Securitised assets like mortgage-backed securities, both in Australia and the US. That theme of higher for longer, structurally higher income, you want to be building into your portfolios in this

new regime and making better use of commodities as a diversifier.

When you say better use of commodities, buying actual commodities, buying ETFs or buying equities in the companies that produce it?

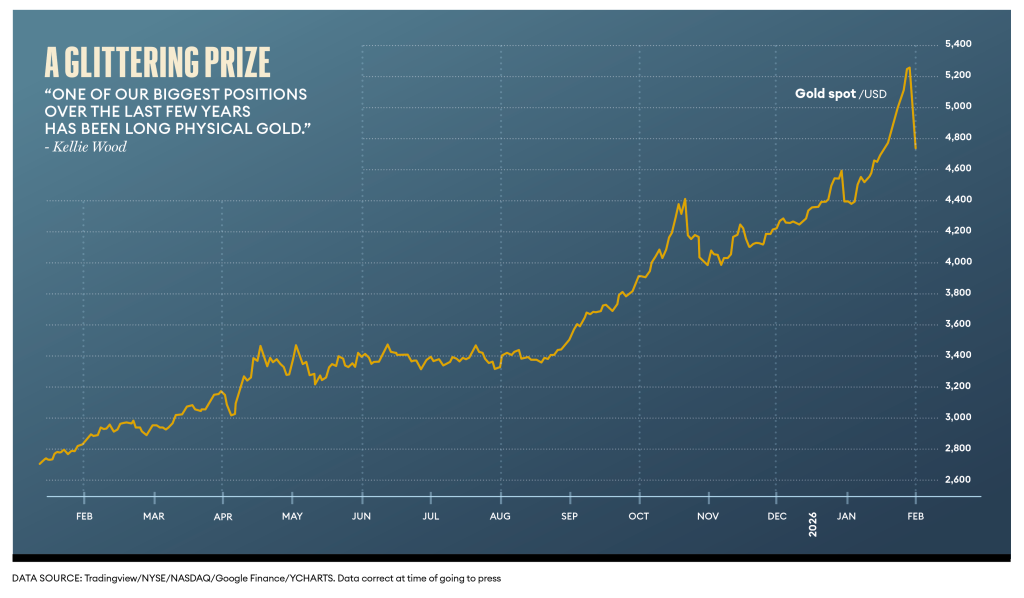

A bit of everything. In a multi-asset portfolio, one of our biggest positions over the last few years has been long physical gold that has been in ETF form, but also buying gold miners globally. Globally, we have an equity strategy that’s been very overweight in gold miners. This also goes towards a lot of investors stepping away from the US Treasury market as a diversifier of equity risk, especially EM, central banks dumping treasuries, and China has been dumping treasuries.

What about equities?

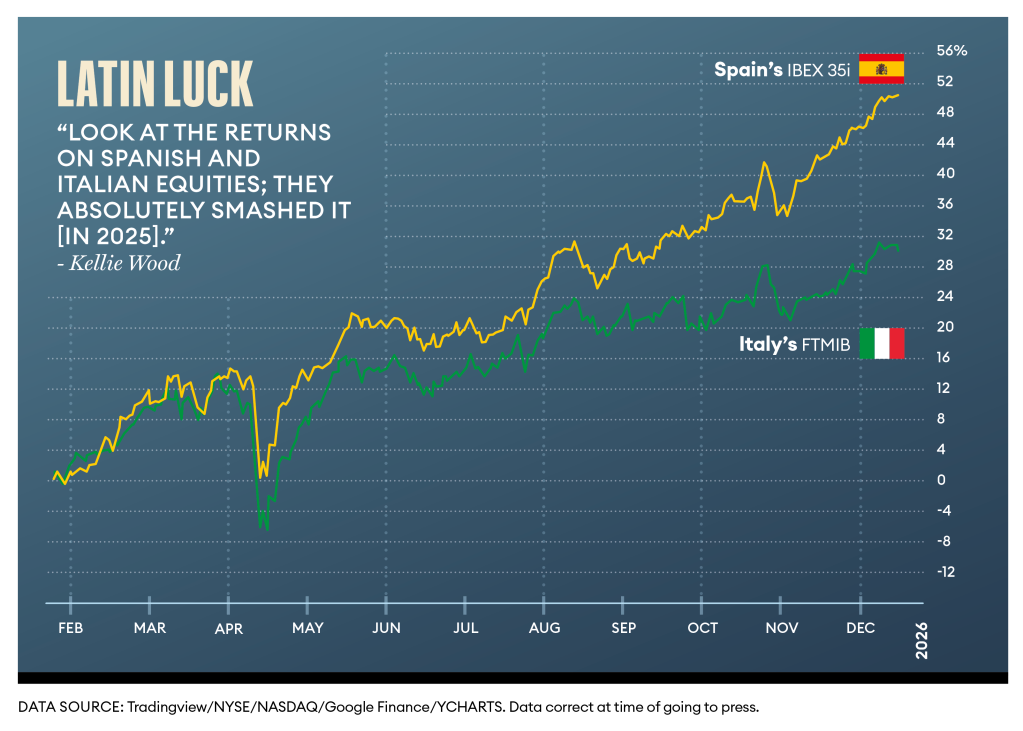

Look at the returns on Spanish and Italian equities; they absolutely smashed it [in 2025] and EM equities. There were a lot of themes around Liberation Day that we were looking to really leverage, moving short US dollars early to capture most of that sell-down. The biggest thing we’ve done in this new regime is just adding in that genuine diversification outside of the US, into EM, into Europe, Spain, Italy, adding in gold, shorting the US dollar. We’ve had a pretty low allocation to Australian equities.

Why is that?

Expensive valuations, but also weaker earnings. You look at tech, and the fundamentals in the US are so much stronger, so there’s a reason why valuations are more expensive.

FI is a broad church. Where are you seeing opportunities, and where are you seeing risk?

If the global economy stays in this soft-landing reflationary environment, which is our view for 2026, the growth holds up, inflation remains sticky, and central banks basically stay on hold, then our preference is still to be owning credit over government bonds – high-quality investment-grade credit in countries like Australia and Europe.

We’re quite short or underweight government bonds in most markets, predominantly the US and Australia – also Europe and Japan. We think there’s a risk here that we see those four central banks re-enter hiking cycles. We’re already seeing it with the Bank of Japan. Europe, we think the next move is up. A lot of our policy modelling in the Fed for the US suggests that that should be at a 3.5% terminal rate.

The risk in government bonds [is] that we see underperformance, and we’ve already started to see that in Australia these last few months, negative returns on Australian government bonds because the market’s gone from pricing easings to hikes. We still prefer securitised assets, so RMBS [residential mortgage-backed securities] in both Australia and the US and emerging market debt.

We’re quite negative on high yield, US hand European high yield.

What about ETFs in this space?

The High Yielding Credit Fund is a strategy that we have been running at Schroders for over 24 years.

In 2024, we decided to launch the fund to external investors as an income product… filling the gap for investors who have traditionally relied on equity dividends for income.

The fund, or HIGH, which is our ETF for the fund, captures the opportunity set across the entire Australian credit space from very high-quality AAA securities through to wholesale sub-investment grade corporate hybrids. The Fund targets 2.5-3% above the RBA cash rate gross of fees. It is differentiated from the majority of ETFs on the market, which focus purely on sub-debt from the banks.

What are the biggest speed bumps you can see in 2026?

The biggest risk is a slowdown in growth [and] weakness in labour markets everywhere. We’ve already started to see it in the US. Labour demand has begun to weaken. Payroll growth in the US is averaging close to zero… and it’s an environment where inflation is still not back within central bank targets, so it limits central banks’ ability to ease policy rates. I think that is what will unravel credit and equity markets: a slowdown in growth with inflation staying sticky, so it’s stagflation lite. That’s probably my biggest concern in terms of the outlook for 2026.

What’s your most optimistic prediction?

US growth tracks between 2 to 3%, inflation sits around 3%. We’re looking at a 5% to 6% nominal growth rate in the US. The consumer continues to be supported by strong labour markets and wealth creation. That’s one reason why we’re still positioned for risk on. Our preference is overweight equities, credit, and alternatives.

What keeps you awake at night?

Weakening growth, stagflation, recession, and ultimately a fiscal crisis. I think that

is definitely what keeps me awake.

Your best piece of advice?

Have conviction. It’s being adaptive and having that sharp macro lens, because that is what will make you money in this new regime.

This article represents the views only of the subject and should not be regarded as the provision of advice of any nature from Forbes Australia. The article is intended to provide general information only and does not take into account your individual objectives, financial situation or needs. Past performance is not necessarily indicative of future performance. You should seek independent financial and tax advice before making any decision based on this information, the views or information expressed in this article.

Want to see more Forbes articles on your feed? Tap here to make Forbes Australia a preferred source on Google.

Look back on the week that was with hand-picked articles from Australia and around the world. Sign up to the Forbes Australia newsletter hereor become a member here.