Ryan Breslow rode his fintech unicorn Bolt to the bank. Then came the lawsuits and money squabbles — and a brutal valuation crash that wiped out much of his fortune.

Silicon Valley ‘King’ Ryan Breslow was dancing barefoot in a geodesic dome when his investors sued him last July.

An aggrieved shareholder was accusing Breslow, the once-billionaire founder of payments unicorn Bolt, of draining millions of dollars from the company by defaulting on a personal loan secured by its cash.

Rather than liquidate his shares to cover the debt, Breslow had allowed $30 million to be swept from Bolt’s bank account, the lawsuit alleged. And when three board members insisted he repay the company, he forced them out instead.

These problems were an ocean away in Ibiza, Spain, where Breslow was headlining a mindfulness retreat centered around dance and “the pursuit of happiness.”

But back home, the suit was among a host of legal battles, bitter money squabbles and shaky ventures that awaited him.

Over the past two years, Breslow has repeatedly attempted to use his Bolt equity to take out large loans, and has tried to expense seven-figure travel and security bills to Bolt after stepping down as CEO, according to internal documents, court filings, and interviews with more than a dozen friends, advisors and colleagues.

One of the companies Breslow cofounded after Bolt, an equity lending platform called Prism, claimed in pitch materials first reported by the New York Times that he had taken out a $100 million loan collateralized by his Bolt shares.

But Forbes has learned the loan was never approved. Three individuals with knowledge of the situation told Forbes that Bolt’s board confronted Breslow after learning of the loan attempt, saying the arrangement would be a violation of his shareholder agreement.

A Prism investor deck viewed by Forbes listed Bolt as a “signed launch partner,” alongside Scale AI, Flexport and Brex.

A spokesperson for Prism told Forbes the company was not aware of the “internal board dynamics” at Bolt, and declined to comment on alleged representations made in pitch materials. “Like any startup, the Prism founding team brainstormed many different concepts before launch, which it refined over time.”

Breslow declined to comment on the Prism loan and a detailed list of questions sent by Forbes saying they contained “too much inaccuracy.”

However, his October 2023 motion to dismiss Activant’s lawsuit confirmed the $30 million loan’s existence and terms, as well as his non-repayment at the time. Bolt declined to comment.

For years, Breslow had personified Silicon Valley success with an archetypal story: a public school kid who dropped out of Stanford University to found Bolt, a one-click payments company that became a venture capital darling and raised $1 billion in funding, earning him a spot on Forbes’ list of the world’s youngest billionaires and a cover story.

When Breslow took out a $30 million loan in November 2021 with unusual terms — if he were to default, Bolt would cover his obligations and could claw back some of his shares as repayment — he was riding high.

By early 2022, Wall Street heavyweights like BlackRock and H.I.G. Growth had lined up to back a $355 million Series E funding round, valuing Bolt at $11 billion and Breslow’s personal stake at over $2 billion.

But instead of catapulting Bolt to new heights, the 2022 deal marked the start of a turbulent 18-month period for Breslow, pocked with acrimonious lawsuits and a showdown with one of Bolt’s earliest backers, Connecticut-based venture fund Activant.

In its July lawsuit, Activant alleged that after being told to reimburse Bolt for the $30 million loan, “Breslow quickly moved to the nuclear option,” forcing out board members Steve Sarracino of Activant, Arjun Sethi of Tribe Capital and Brian Reinken of WestCap, who had tried to compel him to make good on the debt.

Sethi, Tribe, Reinken and WestCap declined to comment.

Florida court records viewed by Forbes show that a month earlier, he changed his middle name to “King.”

Then, between March and April 2023, Breslow installed three new directors — all of them friends.

They included Grammy-award winning producer Larrance Dopson, journalist Esther Wojcicki (mother to Susan Wojcicki and “Godmother of Silicon Valley”), and The Mighty Ducks child actor and crypto investor Brock Pierce.

According to the lawsuit, Breslow said they offered “fresh perspectives and deep networks.”

Breslow has called the Activant litigation “nothing more than sour grapes” over his “unfettered right” to remove members of the board, stating in his dismissal motion that “he did not believe that those directors were the best people to help support his vision for the continued growth and success of Bolt.”

He claimed the loan agreement gave Bolt the option to cancel enough of his shares to repay itself, but the board composed of Dopson, Wojcicki and Pierce decided that such an action “would disallow the Board from pursuing the preferred outcome, ‘restoring the cash.’”

Breslow claimed this board told Activant that he had “proposed alternative structures to the Board for repayment.” It’s unclear what those alternatives were.

The lawsuit is ongoing.

Now, less than a year later, Breslow has already replaced that new board with an even newer cohort of friends that include cofounder of mobile gaming unicorn Playco Michael Carter, former General Catalyst investor Rohan Ram and British-American property developer Joel Schreiber, who was recently caught in a $100 million legal battle with Goldman Sachs and Starwood.

“He absolutely subscribed to his own hype.”

A Bolt investor

Meanwhile, Bolt’s value — which makes up the vast majority of Breslow’s wealth — has crashed.

The company began buying back shares from investors and employees this January at a 97% markdown that suggests a valuation of around $300 million, three sources told Forbes. (This tender offer was previously reported by The Information.)

The offer, which has since ended, also required participants to release Bolt and its affiliates from a broad set of claims.

Forbes has also learned that around the time of the tender offer, Breslow’s $30 million loan debt and several million dollars in expenses were resolved by the cancellation of a number of his Bolt shares, according to two sources with knowledge of the matter.

These sources added that Breslow’s shares were valued at a higher price than those of investors and employees.

At the time of the Series E round, Forbes reported that Breslow owned 22% of Bolt. At the valuation suggested by the tender offer, that stake would be worth an estimated $60 million.

It’s unclear how much of Breslow’s stake was canceled to repay the loan and outstanding expenses.

From young billionaire to ‘clown in the Valley’

Bolt’s 2022 Series E round was an inflection point in Breslow’s life and career. The deal was supposed to set the stage for an anticipated IPO.

And for Breslow, a newly minted billionaire, it was a crowning achievement. Florida court records viewed by Forbes show that a month earlier, he changed his middle name to “King.”

Around this time, Breslow launched a campaign to aggressively expand his empire. Business incorporation filings, real estate records and internal company documents show that by February 2022, he had cofounded four companies, all while remaining Bolt’s CEO.

There was Movement DAO, a blockchain community project; Love Health, an online wellness marketplace; The Movement, a dance nonprofit; and the lending platform Prism.

He’d also self published two instructional playbooks, Fundraising and Recruiting, and had begun shopping for investors in what would become his venture capital fund, Family.

In February, Breslow purchased a second bungalow in Miami, where he’d relocated during the pandemic, and seemed to embrace the trappings of a billionaire lifestyle. Three sources close to Breslow told Forbes that he employed an extensive private security detail.

“It was absurd, a Bill Gates level of security,” said one. The investor recalled Breslow saying that his billionaire status and Forbes cover made him a target. “He absolutely subscribed to his own hype.”

“He cared a lot more about the spoils of being an entrepreneur than the precursors.”

A friend and former Stanford classmate of Breslow

Ten days after Bolt announced its Series E in January 2022, Breslow tweeted a flurry of insults at investors Sequoia Capital and Y Combinator, who he called the “Mob Bosses of Silicon Valley” and accused of colluding with payments competitor Stripe.

Representatives of both firms rejected the claims on Twitter, with Sequoia partner Shaun Maguire calling them a “steaming pile of [poop emoji].”

Six days later, Breslow abruptly stepped down as Bolt’s CEO to become its executive chairman, telling CNBC the decision was his own and had come to him while meditating. (Breslow’s title is now chairman, according to the company.)

The move shocked Bolt’s investors and board members, who had expected its founder to lead the company to an exit via a stock market listing, two sources told Forbes. And it significantly changed his relationship with Bolt.

In an internal company document addressed to Breslow and viewed by Forbes, new CEO Maju Kuruvilla subsequently reminded him that as chairman, his employment status was as an independent contractor and that he was not “to speak on the Company’s behalf including to current or future investors, current or potential customers, or media.”

Then, in May 2022, a New York Times report claimed that Breslow had juiced Bolt’s fundraising and $11 billion valuation on inflated metrics, and not long after the Securities and Exchange Commission began investigating statements he had made around the Series E; it ultimately decided not to take enforcement action.

Kuruvilla told Forbes at the time that Bolt had “put this behind us and we’re focused on continuing to build on our positive momentum.” Still, the incident and Breslow’s general trajectory over the past two years soured some investors and peers who’d previously championed him.

“He became the clown in the Valley,” said one.

Tensions sharpened when Breslow unsuccessfully pressed the board to approve several million dollars in travel and security expenses, three people with knowledge of the incident told Forbes. According to these sources, Breslow claimed the trips were for fundraising purposes.

A separate source familiar with his travels told Forbes he spent much of the summer of 2022 visiting friends across Europe and Egypt, returning home that August to attend the Burning Man festival. The board was unmoved, the three sources added, and denied his request.

“He thinks he can sell anything to anybody,” a friend and former Stanford classmate of Breslow told Forbes. “But he cared a lot more about the spoils of being an entrepreneur than the precursors.”

In September 2022, Breslow had also pressed the board to approve a “moonshot” stock grant plan that was contingent upon Bolt’s growth. When Bolt and Breslow failed to hit their targets, he argued for the targets to be slashed, said one Bolt investor with knowledge of the discussion.

Breslow was denied and the bonus never paid. He declined comment on the incident.

Breslow beyond Bolt

With Bolt officially under new leadership, Breslow’s attention shifted to his other ventures that were demanding more of his time — and money.

In 2021, he had invested at least $16 million into a blockchain startup called Movement DAO, which aimed to democratize the infrastructure for DAOs (decentralized autonomous communities) through which people could crowdfund worthy causes.

Breslow hired former Securities and Exchange Commission contractor Mark Phillips to engineer the project, eventually moving him and two other team members into one of his Miami homes.

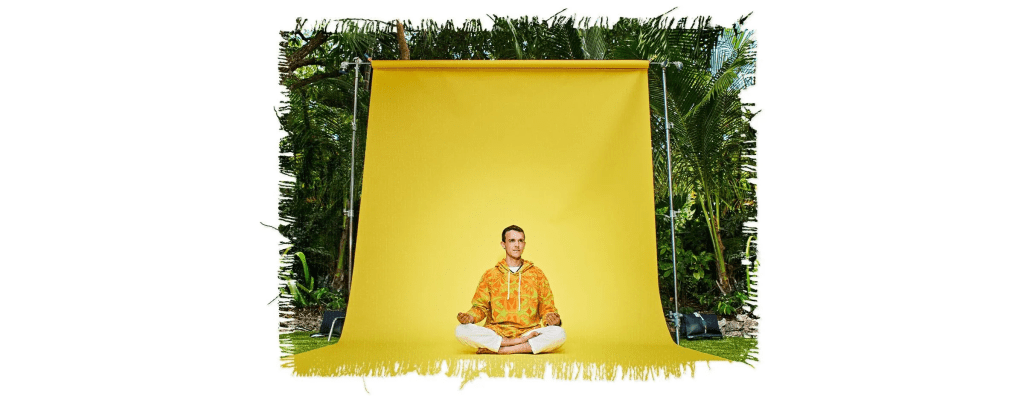

In March 2022, Breslow hosted a launch party for another charitable DAO in Miami’s Venetian Islands. Party photos show Breslow splayed out on a tie dye mat, while a sound healer plays Tibetan singing bowls on his stomach.

But by August 2022, Breslow was itching to recoup his funds, according to a Florida Southern District Court lawsuit in which he had sued Phillips.

The complaint alleged that Phillips, who was given control over the project’s wallets, refused to return Breslow’s millions when asked. (Breslow also claimed that he was unaware Phillips had been previously convicted of federal wire fraud and money laundering in 2011. Phillips replied that he had never hidden his prior conviction, which was easily discoverable through a Google search.)

In a counter-complaint, Phillips alleged that Breslow’s attempts to claw back his donation were a violation of Movement DAO’s bylaws.

The complaint was dismissed last October in a settlement that awarded Breslow roughly $10 million from the DAO’s treasury, and both parties were released of any current and future claims.

Speaking on behalf of Phillips and himself, co-defendant Ben Reed told Forbes, “We are not surprised by Breslow’s continued troubles due to his pattern of questionable behavior and this is why we settled, repaid contributors, and moved on.”

One Bolt investor called Breslow’s manifesto Fundraising “dangerous to young entrepreneurs.”

In June 2023, Breslow again found himself in court when Love Health, an online wellness marketplace he’d originally cofounded as a cryptocurrency pharmaceuticals startup, was sued by The Hills reality TV star Lauren Bosworth, who claimed it infringed on trademarks held by her own company Love Wellness.

The case ended last November in an undisclosed settlement. Bosworth did not respond to a request for comment.

Because Breslow’s wealth was almost entirely tied up in his Bolt stock, in at least one case he used his shares as collateral to bankroll new ventures: In February 2022, he told Bloomberg that he had borrowed against his equity to start The Movement dance nonprofit.

Tax filings show he personally donated a combined $886,310 to the charity in 2021 and 2022. It’s unclear whether the contentious $30 million loan was used to fund any of his other companies.

His most recent project, the venture capital fund Family, was quietly downsized from $140 million to a more modest $40 million, Axios first reported. Its first investment: a male birth control startup titled Life Sciences.

‘We’re never going back’

When Breslow’s bills started coming due, he struggled to manage them. In November 2022, with just three months until the $30 million repayment deadline, Breslow asked his previous board for an extension, Activant claimed in its lawsuit.

That same month, the company terminated 29% of its workforce in a second round of layoffs for the year, citing a need to “secure our financial position, extend our runway, and reach profitability with the money we have already raised.”

The cuts were uniquely painful for some Bolt workers who had taken advantage of a plan that Breslow had concocted, allowing them to borrow money from Bolt to buy vested shares.

In deleted tweets from February 2022, he had described the initiative as “the most employee-friendly stock option program possible,” and claimed that more than half of Bolt’s employees chose to participate. Then, suddenly, laid off staff had just 90 days to repay their debts.

A Bolt spokesperson said at the time that only a “single-digit” number of sacked workers were affected.

Breslow’s plucky origin story which once headlined Bolt’s website has been quietly removed.

Two months after the layoffs, Breslow told the board he would be defaulting on his own loan, and in February 2023, millions were swept from Bolt’s account.

Now Breslow, who has since moved to Los Angeles according to three people in touch with him, is facing a reckoning of his legacy at Bolt.

Its novel four-day work week program, which he proudly announced in September 2021 — saying, “we’re never going back” — was killed earlier this year, according to an staff memo viewed by Forbes (the memo characterized the change as “creating more space” for “not only work but opportunities for our teams to connect with each other.”)

Investors had previously told the company that it was a distraction causing Bolt to drift away from its core business, according to internal communications viewed by Forbes.

His reputation as an entrepreneur and visionary has also taken a hit. One Bolt investor called Breslow’s manifesto Fundraising “dangerous to young entrepreneurs.”

A founder and friend of Breslow told Forbes they had warned “so many people not to follow his fundraising method,” believing it valued ego and storytelling above pitching an actual product.

Even Breslow’s plucky origin story which once headlined Bolt’s website has been quietly removed. Meanwhile, Activant is pressing Bolt to open its books for potential evidence of “waste” and “self dealing.”

In response to the investor’s rights request, however, Bolt returned only six documents. The company hasn’t yet responded to these allegations.

With his twenties nearly behind him, Breslow’s next act is shaping up to be, perhaps, a bit more staid.

At his 29th birthday celebration last May in Guanajuato, Mexico, accommodations at a luxury wellness resort were “graciously provided by Ryan,” according to an invitation seen by Forbes. This year’s celebration will be different.

Attendees have been told they’ll be footing the bill for their lodging, though at a discounted rate if they use the code “BRESLOW.”

This article was first published on forbes.com and all figures are in USD.