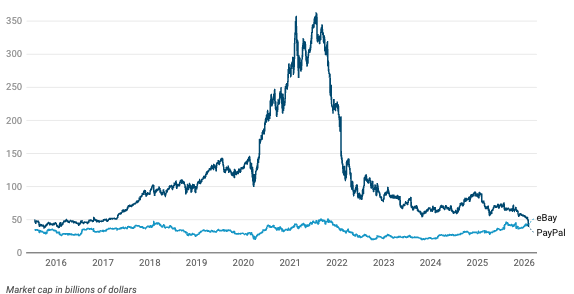

For the first time since the companies split in 2015, the former subsidiary has a smaller market value than its old parent. eBay’s market cap is about $42 billion. PayPal’s has fallen to roughly $40 billion.

Rising competition from a bank-backed rival has put pressure on PayPal’s payments business and its stock. (Photo by Justin Sullivan/Getty Images)

Getty Images

PayPal is now worth less than eBay.

That shift came after PayPal’s shares fell 17% Tuesday. The stock is down about 85% over the past five years and now trades at its lowest level since 2017. The drop followed a disappointing earnings report. PayPal said revenue of $8.68 billion and earnings of $1.23 a share both came in below Wall Street forecasts of $8.8 billion and $1.28 a share, respectively. The company said online spending slowed and competition intensified, particularly from Apple Pay. It also cut its outlook for profit growth this year to the low single digits, well below expectations of about 8%.

eBay bought PayPal in July 2002 in an all stock deal valued at about $1.5 billion. Back then, eBay needed a way for buyers and sellers to move money online. PayPal provided that service. Payments grew faster than auctions. Investors later argued that the two businesses would perform better on their own. The companies split in July 2015.

For years, PayPal looked like the clear winner. At the time of the split, eBay was valued at about $35 billion. PayPal was worth about $49 billion. During the pandemic boom in July 2021, PayPal’s market cap climbed to about $360 billion pushing the gap between the two companies to a record $315 billion while making PayPal eight times larger than eBay.

From Lead to Lag

For the first time since the two companies split, eBay has a higher market capitalization than PayPal

But the payments market has become crowded with competition.

While PayPal was an early 2000’s winner, Apple Pay, Google Pay, Stripe and Zelle are now duking it out for market share. That’s most pronounced in personal payments. Zelle, a person to person payments service owned by major U.S. banks, launched in 2017. In its first full year, Zelle processed $119 billion in payments, nearly double PayPal’s peer to peer app Venmo, which handled $62 billion. That two to one ratio held for several years, but by 2023 Zelle handled about $800 billion in transactions compared with Venmo’s $276 billion. Today the gap has only grown wider. Zelle processed more than $1 trillion in annual volume in 2024 with expectations that they’ll announce $1.2 trillion in volume in 2025, while Venmo handled about $320 billion in 2025. Given the ubiquity of reliable payments options, most consumers have stopped thinking about which company handled transactions. PayPal still processes large volumes of payments, but fewer shoppers actively choose it at checkout.

Now PayPal is looking for a new role. The company announced a leadership change this week and said execution has fallen short of expectations. Management is turning to artificial intelligence as a way to restart growth. Analysts call the approach “agentic commerce.” What that means is using AI to guide shoppers from search to payment in one continuous process.

Canaccord Genuity, the Canadian investment bank, said in a January report that this could be PayPal’s most promising idea since its time inside eBay. The firm pointed to PayPal’s network of merchants and consumers as a key advantage. Merchants can connect once and reach several AI platforms. Moving from an AI search result to checkout could take only a few clicks. The analyst said agentic commerce could become PayPal’s best use case since, well, eBay.

All of that depends on a market that doesn’t yet exist at scale. Investors, meanwhile, are pricing PayPal based on slower growth and tougher competition today.

PayPal was built to help strangers buy and sell things on eBay. Now the market is treating PayPal itself like a second-hand knickknack, repriced after years of competition and slower growth. The bet on artificial intelligence is an attempt to create a new reason for PayPal to matter in online commerce. Until that story proves out, the stock looks less like a growth company and more like something waiting for its next bidder.

This article was originally published on forbes.com and all figures are in USD.

Look back on the week that was with hand-picked articles from Australia and around the world. Sign up to the Forbes Australia newsletter here or become a member here.