The global mining and metals industry has pivoted from a volume-driven commodity rush to a strategic chess game, increasingly influenced by a paradigm shift in the geopolitical order. Resources are mined once, but value is added many times. Data journalist Juliette O’Brien examines where Australia captures value in its key minerals – and where it leaves it to others downstream.

This story features in Issue 23 of Forbes Australia. Tap here to secure your copy.

The ground beneath Australia’s resources is shifting. As capital pours into clean energy and AI, a global race is underway to supply the metals that underpin both.

Australia has an abundance of natural resources. But this race is about more than volume; it’s about adding value, with the biggest gains flowing to countries that turn raw resources into refined metals, chemicals and manufactured products.

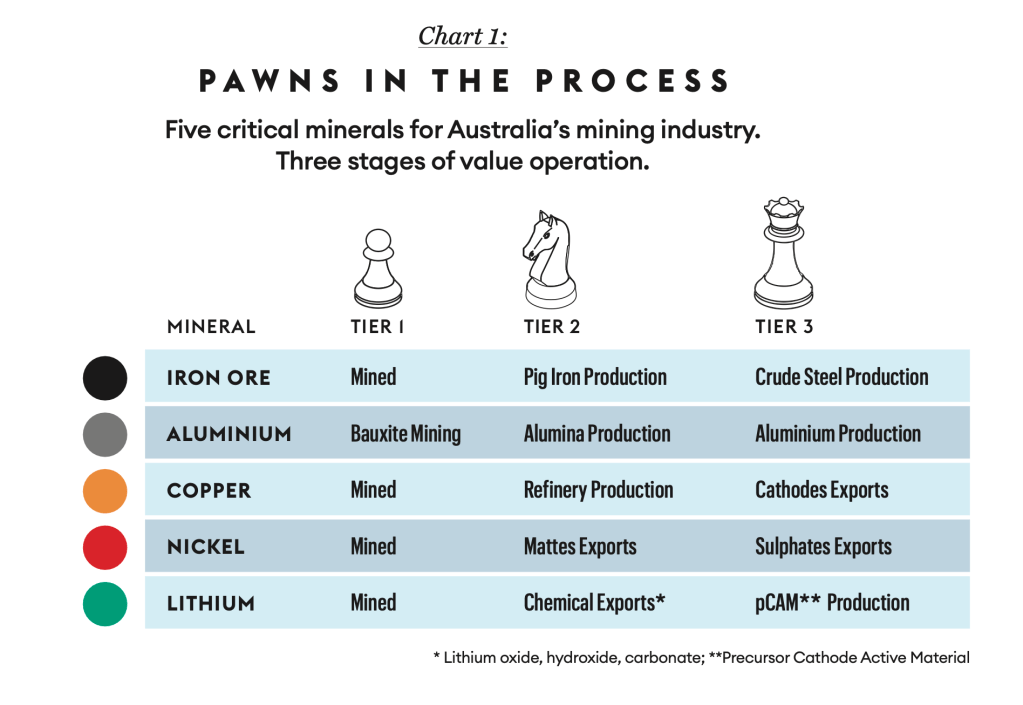

A Forbes Australia analysis mapped five major Australian commodities across the value chain: iron ore, aluminium, nickel, copper and lithium. It distils these complex markets into three broad tiers: mining and extraction; refining and intermediate processing; and more advanced manufacturing or fabrication.

For more complex value chains, the analysis uses selected key products as proxies. Each metric draws on comparable global data, using production figures from the U.S. Geological Survey’s (USGS) Mineral Commodity Summaries or export values from the World Bank.

Australia’s strength is clearly as a quarry, rather than a processor. It leads the world in the extraction of two of the five selected minerals: iron ore and lithium. But it does not rank first in any downstream stage of value-adding. (Chart 1)

China tells the opposite story. It leads the world in six categories across four minerals, all of them downstream. Guinea and Chile join Australia as mining leaders, extracting the most bauxite and copper, respectively. But Chile also reaches further down the chain, leading in selected advanced copper and lithium products. Indonesia dominates every stage of the nickel market.

The number-one ranking only tells part of the story. The scale of the imbalance is clearest in iron ore. Australia is an iron ore giant, producing an estimated 980 million tonnes (Mt) of iron ore in 2025 – 38% of the global total, according to the USGS. China, however, captures most downstream activity, producing 830 Mt of pig iron (tier 2) and 964 Mt of crude steel (tier 3). (Chart 2). Australia’s Department of Industry, Science and Resources reports crude steel production in 2025 was 4.9 Mt – tiny by global standards. The result is Australia sells iron ore, then buys back steel.

Aluminium tells a somewhat brighter story. (Chart 3) Australia ranks second in the world for bauxite mining and alumina production. It is also a significant aluminium producer, ranking seventh globally, but still trails China, India, Russia, Canada, the UAE and Bahrain – countries where abundant energy supports energy-intensive smelting.

Nickel is a case study in vertical integration on a national scale, with Indonesia muscling its way into the entire value chain. (Chart 4). Using exports of nickel mattes (an intermediate product created by smelting nickel ore) and nickel sulphates (a highly pure chemical compound used in manufacturing) as proxies, Indonesia ranks first across all three tiers. The regional heavyweight has flooded the market, pushing prices to five-year lows and crushing mine profitability for higher-cost producers. In Australia, nickel mine production plunged 54% in 2025.

Copper’s value chain is far more geographically distributed. Mining is concentrated in Chile and Congo, while refining is dominated by China. (Chart 5). Chile is also the world’s largest exporter of copper cathodes (a highly pure form of refined copper used to make products such as wire and cable). Australia has strong industries across all three tiers, ranking eighth for mining, thirteenth for refining, and fifth for copper cathode exports. As of December 2025, refined output was rising faster than mined output, indicating a move further down the value chain.

Lithium may be Australia’s biggest downstream opportunity. Australia is the mining leader, producing 92,000 tonnes of lithium content in 2025 – 32% of the global total, according to the USGS, largely from spodumene extraction. (Chart 6) Chile leads exports across the selected basket of refined lithium chemicals: lithium oxide, hydroxide and carbonate. China produces 95% of the world’s precursor cathode active material (pCAM), a processed powder used to make lithium-ion battery cathodes, according to Benchmark Mineral Intelligence and the International Energy Agency.

Australia currently ranks sixth for lithium oxide/hydroxide exports, with production rising. The Department of Industry, Science and Resources expects lithium hydroxide output to increase fivefold by 2027, supplying 9% of the global market. This may be evidence that Australia is moving beyond the quarry model.

The next phase of the minerals race will test whether Australia can capture more of the value built on its own resources or keep digging while others move downstream.

Data sources: Benchmark Mineral Intelligence; International Energy Agency; Resources and Energy Quarterly, December 2025, Department of Industry, Science and Resources; Mineral Commodity Summaries, February 2026, U.S. Geological Survey; World Integrated Trade Solution (WITS), The World Bank.

This article represents the views only of the subject and should not be regarded as the provision of advice of any nature from Forbes Australia. The article is intended to provide general information only and does not take into account your individual objectives, financial situation or needs. Past performance is not necessarily indicative of future performance. You should seek independent financial and tax advice before making any decision based on this information, the views or information expressed in this article.

Want to see more Forbes articles on your feed? Tap here to make Forbes Australia a preferred source on Google.

Look back on the week that was with hand-picked articles from Australia and around the world. Sign up to the Forbes Australia newsletter here or become a member here.