The AI-native ecosystem grew 969 per cent between 2021 and 2025, according to Startup Genome’s new global report. Almost 90 per cent of that funding landed in North America, predominantly in Silicon Valley and New York. Here’s where Australia’s innovation hubs rank.

Unsurprisingly, the Bay Area and the Big Apple are the undisputed epicentres of AI-native tech investment. Third on Startup Genome’s new AI-native funding list is Beijing.

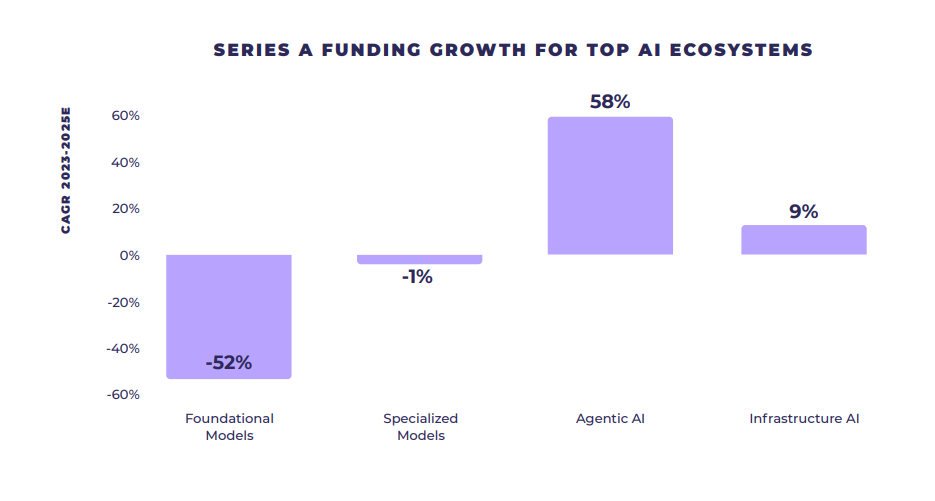

Globally, some $21 billion in Series A funding was pumped into AI-native startups in 2025, an uptick of 17 per cent from the year before. And, while it might be Silicon Valley’s foundational models, Anthropic and OpenAI, that first come to mind as the big fundraisers in 2026, the research reveals that last year, it was Agentic AI companies raising seed and Series A rounds that sucked up much of the capital.

This accelerated allocation of dollars into agentic AI startups – that don’t create AI models and instead layer third-party AI into a startup to solve industry-specific challenges – made a big difference to the startup ecosystem rankings for cities around the world.

Series A funding for those startups has grown 58 per cent a year over the last two years. Overall, AI-Native businesses account for 45 times as many startups, according to the Startup Genome report, as well as 9x as many seed deals and 5x as many Series A deals.

This is not just true in the US. London, Tel Aviv, Boston, LA, Beijing, Singapore, Seoul and Seattle rounded out the Top 10, after the Valley and NYC.

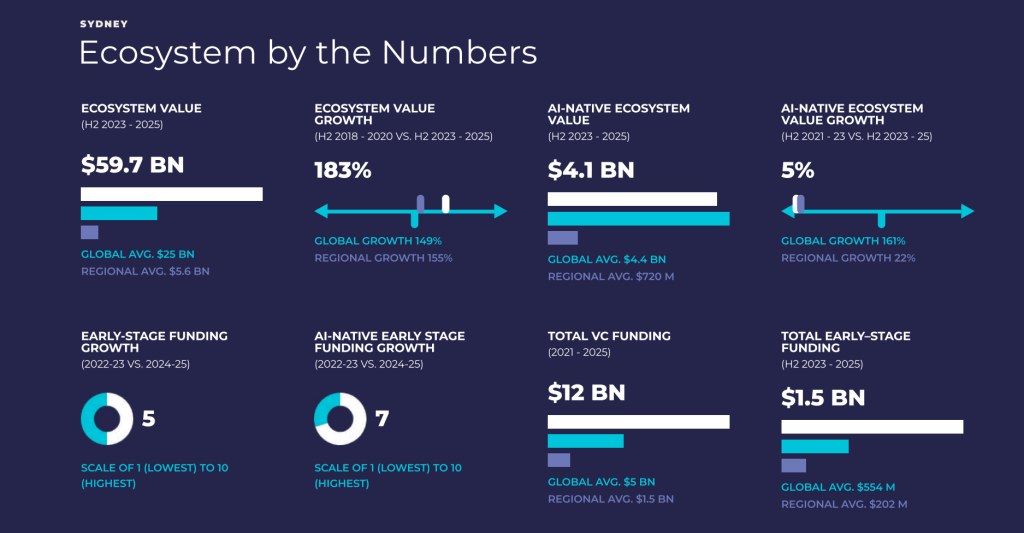

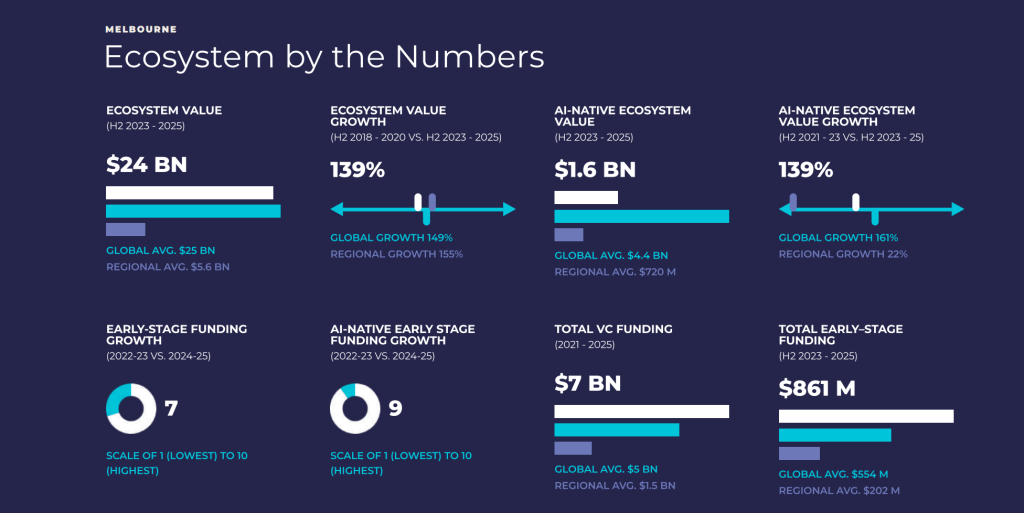

So, where does Australia sit in all of this? The answer is well down the list. The 2026 rankings – which reflect what happened in 2025 – reveal that Sydney is the strongest ecosystem in Oceania, and held on to the 26th spot. Melbourne moved up two places and now sits in 30th place. Brisbane was not in the top 40 list of cities globally but placed fourth in Oceania, after Auckland.

Top 20 Global Startup Ecosystems

Global Startup Ecosystem Ranking

GSER 2026 — Top 20 Ecosystems| Ecosystems ▲ | Overall Ranking ▲ | Performance ▲ | Funding ▲ | Talent & Experience ▲ | Market Reach ▲ | AI-Native Cluster ▲ | R&D Engine ▲ | Improvement from GSER 2025 ▲ |

|---|

Source: Global Startup Ecosystem Report 2026

Impressive, no doubt, for a country of just 28 million people.

But Startup Genome's report raises the question: how can Australia, which lacks the heft of US tech companies' foundational models, best excel in this new AI-native, agentic world? How do our founders compete for capital that is going to places they are not located?

Rewriting the capital and sector rule books

Our nation's total ecosystem value has expanded at the fastest clip of any nation over the last decade, marking a distinct transition from 2016 when local startups were rarely factored into global tech conversations. International success stories Canva, Atlassian, Airwallex, and other tech unicorns have driven that growth.

The latest global data marks a fork in the road. SaaS still plays a vital role, but venture capital is increasingly concentrating around applied, deep, defensible intellectual property rather than purely digital applications. Artificial intelligence is transitioning from pure 'software' into a general-purpose technology embedded into physical industries. These are cost-intensive sectors that require vast amounts of R&D and a visible hand to make the transition to this new frontier.

"The role of the state is expanding," Startup Genome's report states. "Governments are increasingly acting not only as regulators but also as investors, customers, and ecosystem architects, particularly in sectors which are strategically important and capital intensive, such as AI infrastructure, semiconductors, defense, and quantum technologies."

This macro global trend suggests Australia's Deep Tech and Advanced Manufacturing sectors - which have historically been supported by incubators like Cicada Innovations, universities, and VCs Main Sequence and Blackbird - are becoming more crucial.

In 2026, startups in this space can now also look to the federal government, specifically the recent trend to use R&D tax credits as a ‘raise alternative’ and tapping into the $1 billion pool available under the $15 billion National Reconstruction Fund Corporation (NRFC). Those initiatives put Australia in step with the ‘future-proofing’ analysis that Startup Genome outlined this week.

"The ecosystems that are pulling ahead are those able to mobilise capital at scale, integrate frontier technologies, and align public and private actors around strategic priorities," the report reads. "Others face a growing risk of experiencing the disruptive effects of technological change without capturing its economic benefits."

One nation that excels in deploying public capital is China, which recently launched a national VC fund worth more than US$21 billion, focused on AI, semiconductors, quantum computing, aerospace, biomedicine, and advanced next-generation communications technologies.

In the Australian arena, Queensland's capital city is an emerging hotspot, due to its burgeoning aerospace industry led by homegrown success stories Gilmour Space and Hypersonix, both of which recently raised significant rounds that included funds from the NRFC.

The city was called out in the Startup Genome report as a "critical hub for global space commercialisation" and an emerging market "cementing its role as a leader in aerospace and space innovation, driving breakthroughs in autonomous systems, robotics, AI, and hypersonic technology."

Deep tech drawing private and public funds to grow

Syenta is another strong example of an Australian startup on the rise. In April of this year, the ANU spin-out closed a $37 million Series A co-led by the Australian Government's NRFC and Silicon Valley’s Playground Global. Pat Gelsinger, former CEO of Intel, subsequently joined Syenta’s board to support international expansion and the launch of US manufacturing operations in Arizona.

But getting Syenta to the point that the government and a Palo Alto VC will lead a Series A, is no easy task. It would not have been possible without Australia's Blackbird Ventures, Jelix Ventures and Brindabella Capital putting together a seed round in 2022. Investible, OIF Ventures, Salus Ventures, Robyn Denholm’s Wollemi Capital Group, Singapore’s SGInnovate, and Arlington, Virginia-based intelligence VC In-Q-Tel contributed to the pre-series A.

Syenta’s growth path reflects how vital seed capital is to enable audacious, sovereign-defining ideas. Blackbird partner Niki Scevak was one of the very first to spot the value in Syenta's hardware and to put up funds to enable it to flourish.

While the semiconductor startup led by co-founder CEO Jekaterina Viktorova is a guiding light, it is also a rarity. And that is something to think about as we move into 2027 and beyond.

"While this year’s ranking shows less disruption than last year’s, these forces are driving a shift away from the more globally-distributed innovation landscape of the last decade, toward one that is increasingly concentrated, strategic, and politically mediated," the report concludes.

"The global startup ecosystem is being reshaped by the rise of Artificial Intelligence, the growing influence of geopolitics, and a marked expansion in the role of the state."

10 pillars of Australian Deep Tech

As the global ecosystem expands toward deep IP, a distinct group of highly specialised engineering, aerospace, and biotech companies has emerged, adding new dimensions to Australia's innovation landscape.

Space & Hypersonic Aerospace

1. Gilmour Space Technologies (Gold Coast, QLD): Developing sovereign orbital launch vehicles and managing its own spaceport in Bowen. The company secured an A$217 million Series E round co-led by the NRFC and Hostplus, marking a significant milestone for local aerospace infrastructure.

2. Hypersonix Launch Systems (Brisbane, QLD): Focusing on scramjet engines and unmanned hypersonic vehicles designed to travel at high speeds using 3D-printed alloys. The team has secured prime development contracts with the US Department of Defense's Silicon Valley arm.

Robotics & Autonomous Marine Systems

3. Advanced Navigation (Sydney & Newcastle, NSW): Manufacturing high-end navigation systems and underwater robotics. The company expanded its physical production footprints in Newcastle following a US110 million (A165 million) Series C round, which included a A$50 million investment from the NRFC.

4. Carbonix (Sydney, NSW): Manufacturing long-range, industrial-grade vertical take-off and landing commercial drones from advanced composite materials. They have partnered with major aerospace and defense tier-ones to integrate their aerial platforms into commercial fleets.

Climate Tech & Chemical Engineering

5. MCi Carbon (Newcastle, NSW): Utilising chemical engineering to capture carbon emissions from heavy industrial plants and permanently transform them into physical building materials. Their work is backed by a A14.6 million federal grant and corporate equity from industrial partners like RHI Magnesita.

6. Hysata (Wollongong, NSW): Developing ultra-high-efficiency hydrogen electrolyzers aimed at lowering the cost of green hydrogen production. The company is scaling operations within its gigawatt-scale facility after closing a US111 million (A$167 million) Series B round co-led by bp Ventures and Templewater.

Biotech & Biological Computing

7. Synchron (Melbourne, VIC): Developing implantable brain-computer interfaces designed to help paralyzed patients interact with digital devices via thought. Backed by international investors including Jeff Bezos and Bill Gates, they continue to scale up clinical manufacturing.

8. Cortical Labs (Melbourne, VIC): Investigating biological computing by integrating live biological neurons onto silicon computing chips. The company raised a US$10 million round led by Horizons Ventures to transition their research into commercial testing arrays.

Microchips & Quantum Architecture

9. Diraq (Sydney, NSW): Engineering utility-scale quantum computing processors using existing silicon semiconductor infrastructure. To further their development, they secured an A$20 million strategic equity investment from the NRFC.

10. Li-S Energy (Brisbane, QLD): Manufacturing next-generation Lithium-Sulfur batteries that incorporate Boron Nitride Nanotubes for aviation and transit applications. Publicly listed on the ASX, they have established product co-development agreements with international aerospace partners.

Want to see more Forbes articles on your feed? Tap here to make Forbes Australia a preferred source on Google.

Look back on the week that was with hand-picked articles from Australia and around the world. Sign up to the Forbes Australia newsletter here or become a member here.